And unfavourable on the 2s10s:

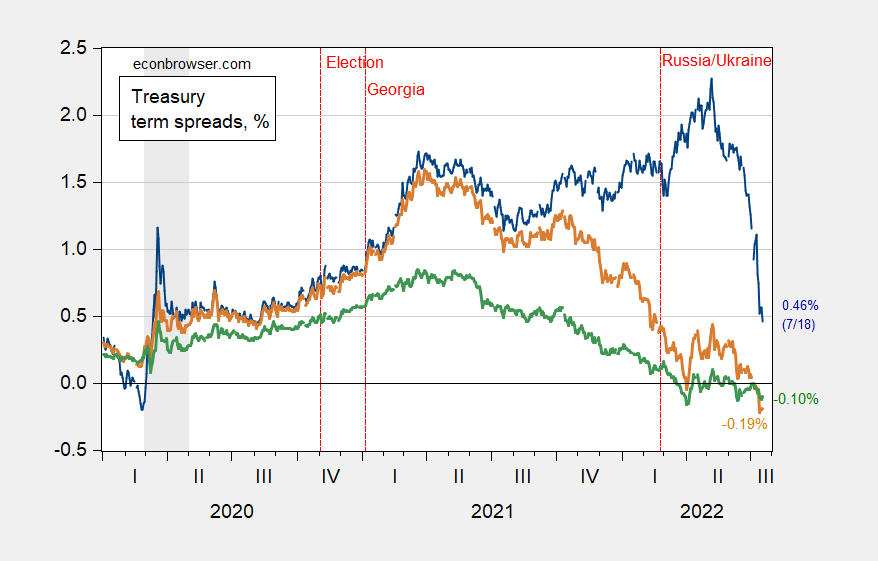

Determine 1: 10yr-3mo Treasury unfold (blue), 10yr-2yr (tan), and 10yr-5yr (inexperienced), all in %. NBER outlined peak-to-trough recession dates shaded grey. Supply: Treasury by way of FRED, writer’s calculations.

The drop within the 10yr-3mo unfold is sort of precipitous. For me, that is the very best (single) predictor for recession on the 12 month horizon.

The truth that the 2s10s and 5s10s are unfavourable highlights the truth that the inversion is on the center of the spectrum.

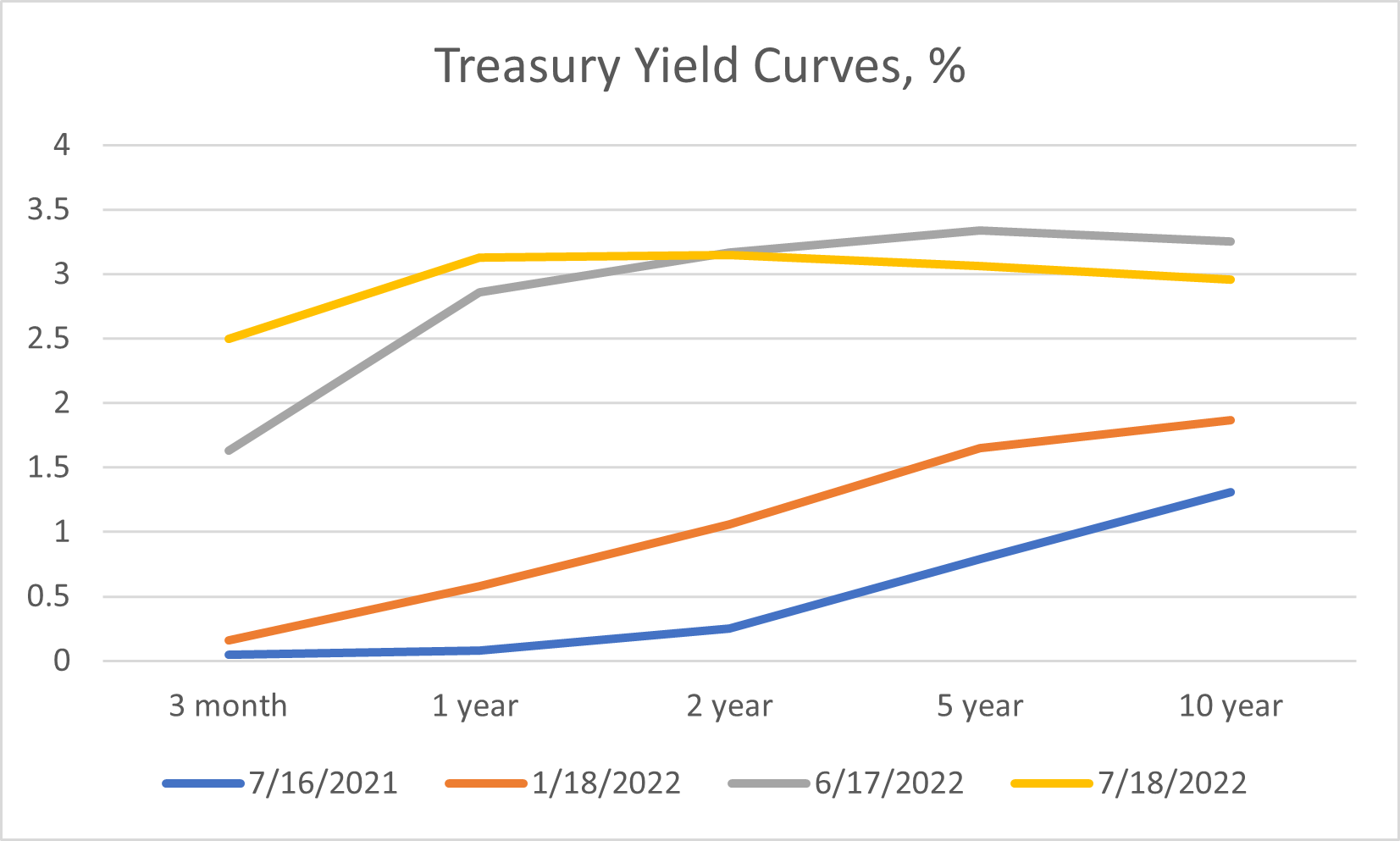

Determine 2: Treasury yield curves, as of indicated dates, in %. Supply: Treasury by way of FRED.

As of a month in the past, the yield curve was usually upwardly sloping, though the 10s5s was unfavourable. As of shut right this moment, we have now an inversion between 3 years and 20 years (not proven).

{kind=link}