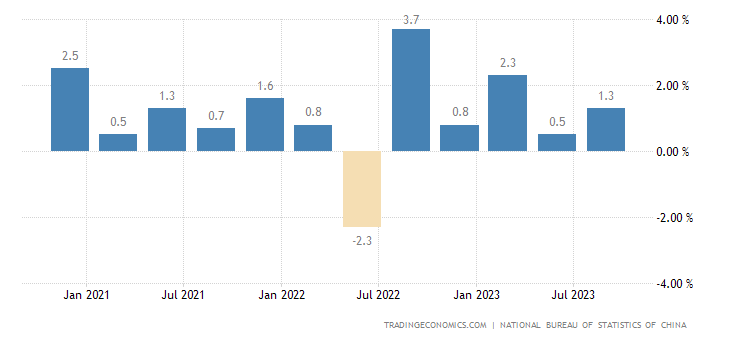

Q/Q was 1.3% vs. consensus 1%.

Supply: TradingEconomics.

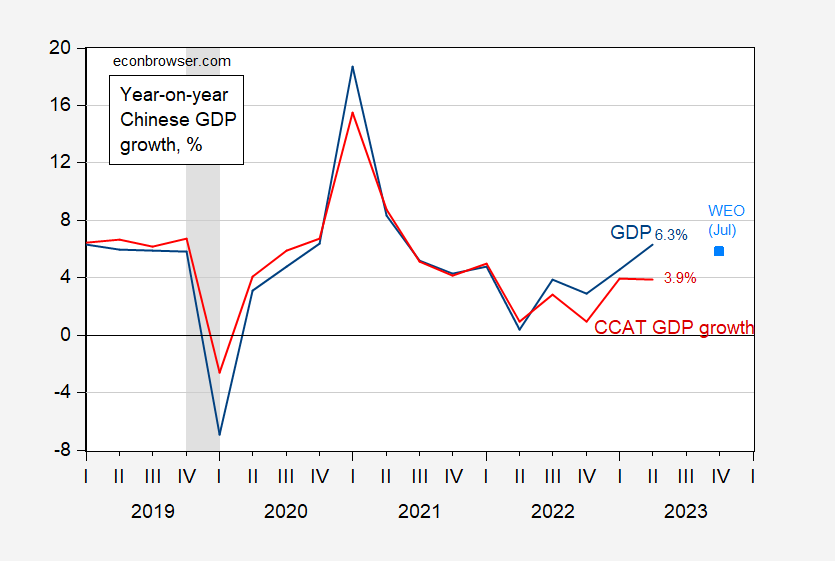

Some skepticism is warranted, given CCAT’s implied numbers for Q2 (on a year-on-year foundation), mentioned on this publish:

Determine 2: Yr-on-Yr Chinese language GDP development (blue), and development implied by China CAT (crimson), IMF WEO July forecast (sky blue sq.). ECRI outlined peak-to-trough recession dates shaded grey. Supply: NBS, private communication, IMF WEO July replace, ECRI and writer’s calculations.

Natixis wrote yesterday:

Regardless of the encouraging momentum, three regarding components are nonetheless at play. First, mounted asset funding in actual property continued to edge downward to -9.1% in September from -7.9% in June, posing considerations concerning the potential spillover impact on the sector, together with native governments’ funds. Second, the CPI stays hovering round 0%, which indicators stagnant demand. Third, China’s geopolitical relationship with the West stays a priority, particularly after the US’ resolution to tighten export controls on China.

{kind=link}